Data Center Construction Market Size, Status and Industry Outlook During 2032

Introduction

The Data Center Construction Market focuses on building, expanding, or upgrading physical infrastructure that houses data center facilities. It includes site development, civil works, structural elements, power and electrical systems, mechanical systems (cooling, HVAC), networking, and finishing works tailored to co-location, hyperscale, enterprise, and edge facilities.

This market holds global strategic importance. As demand for cloud services, edge computing, artificial intelligence, and digital transformation surges, data centers become critical backbone infrastructure. Their construction ties directly to national competitiveness, sovereign data sovereignty, and energy and sustainability planning. In 2024, this market is estimated at approximately USD 240.97 billion and is projected to expand to about USD 456.50 billion by 2030 at a CAGR of 11.8%. Grand View Research

Learn how the Data Center Construction Market is evolving—insights, trends, and opportunities await. Download report: https://www.databridgemarketresearch.com/reports/global-data-center-construction-market

The Evolution

Data center construction has progressed in waves aligned with technological, economic, and digital transformations:

-

In earlier decades, data centers were built ad hoc by corporations or government agencies—small, custom, and often inefficient facilities.

-

The rise of enterprise-scale IT in the 2000s led to dedicated data center builds with better design standards.

-

The emergence of cloud and hyperscale operators (like Amazon, Microsoft, Google) pushed standardization, modular design, and large-scale campus builds.

-

Over the last decade, prefabricated modules, containerized data halls, and edge micro-data centers have reduced construction time, cost, and complexity.

-

Most recently, demands from AI and high-performance computing (HPC) have imposed new requirements: higher power density, advanced cooling (immersion, liquid cooling), flexible floor loading, and renewables integration.

Shifts in demand and technology mean that modern data centers are no longer just about stacking servers—they must incorporate sustainability, reliability, energy efficiency, and future scalability.

Market Trends

Key trends shaping data center construction include:

-

AI and compute density demands: The need for AI-ready data centers is growing rapidly. Demand for AI-ready capacity is expected to rise at about 33% annually between 2023 and 2030. McKinsey & Company

-

Modular and prefabricated construction: Use of prefabricated modules, containerization, and modular design speeds deployment and improves predictability.

-

Edge data center growth: More small or micro data centers closer to end users to reduce latency, especially in 5G/IoT environments.

-

Sustainability and energy optimization: Integration of renewable energy, heat reuse, efficient cooling (direct liquid, immersion), and carbon footprint reductions.

-

Liquid cooling and immersion cooling: To handle high power densities, new cooling techniques are being adopted.

-

Tier standards and resilience: Many new construction projects target Tier 3 or even Tier 4 levels of redundancy and availability.

-

Regional expansion: Asia-Pacific, Latin America, Middle East & Africa are aggressive growth areas for data center construction.

-

Supply chain and component lead times: Long lead times for critical equipment (transformers, switchgear, custom racks) are influencing construction schedules and inventory strategies.

-

Power constraints & grid partnerships: Site selection increasingly aligned with availability of reliable, low-cost, and clean power sources.

Adoption patterns show mature markets (North America, Europe) focusing on upgrades and densification, while emerging markets focus on new builds.

Challenges

The data center construction sector faces multiple challenges:

-

High capital intensity: The cost of land, power infrastructure, cooling systems, and specialized equipment is substantial.

-

Power scarcity and grid constraints: Many regions face limitations on available power, forcing delays or reliance on expensive backup power.

-

Regulatory and permitting barriers: Zoning, environmental approvals, water usage permits, and local compliance can delay projects.

-

Lead time and supply chain risk: Long delivery times for critical components can extend schedules by months.

-

Technological obsolescence risk: Rapid changes in technology may render parts of a facility obsolete before payback.

-

Sustainability compliance: Meeting strict emissions, energy efficiency, and ESG requirements demands additional cost and design complexity.

-

Talent and construction expertise: Building modern data centers requires specialized engineering, integration, and project management skills that are in short supply in many regions.

Risks include macroeconomic slowdowns, energy price volatility, regulatory changes on data or energy, and material cost inflation.

Market Scope

Segmentation by Facility Type

-

Hyperscale Data Centers

-

Colocation / Multi-tenant Data Centers

-

Enterprise / Private Data Centers

-

Edge / Micro Data Centers

Segmentation by Infrastructure Component

-

Electrical Infrastructure (UPS, generators, switchgear, power distribution)

-

Mechanical / Cooling Infrastructure (HVAC, chillers, immersion, liquid cooling)

-

Structural & Civil Construction

-

Networking / Cabling / Interconnect

-

General Finishes & Interiors

Segmentation by Tier / Performance Level

-

Tier 1 / Tier 2

-

Tier 3

-

Tier 4

By Power Density / Deployment Scale

-

Standard density (low to moderate kW per rack)

-

High-density / AI / HPC (tens to hundreds of kW per rack)

By Region

-

North America

-

Europe

-

Asia-Pacific

-

Latin America

-

Middle East & Africa

End-User Verticals

-

Cloud Service Providers / Hyperscalers

-

Telecommunications / 5G Networks

-

Financial Services / Banking / FinTech

-

Government / Public Sector / Defense

-

Healthcare / Life Sciences

-

Research / High-Performance Computing

-

Enterprises (Retail, Manufacturing, Media, etc.)

Regional Analysis & Adoption Patterns

-

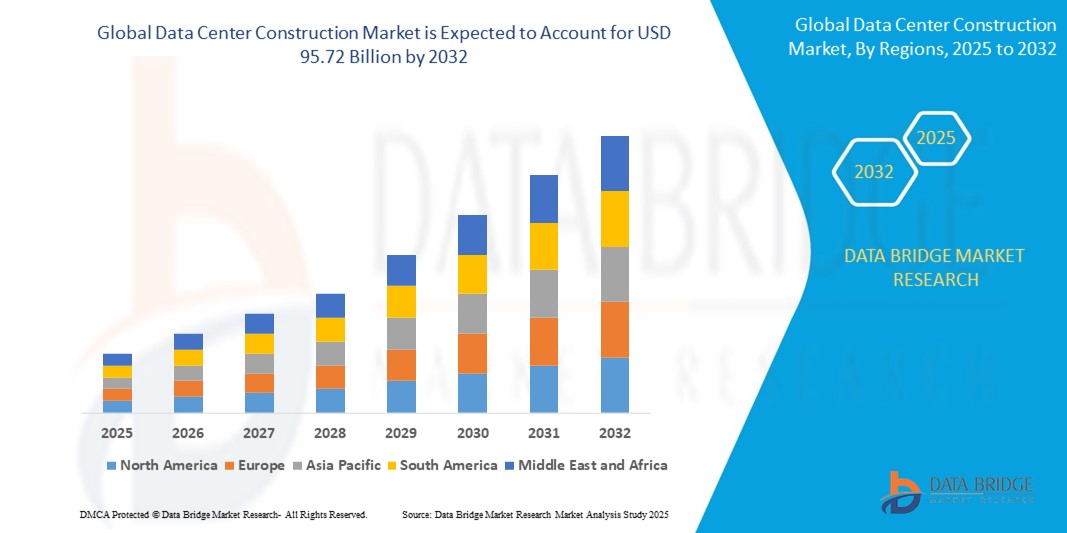

North America is the largest region in data center construction, holding over 40% of market share as of 2024. Grand View Research+1 Many hyperscalers and cloud providers are U.S.-based and continue to expand regionally.

-

Asia-Pacific is fastest-growing, with China, India, Southeast Asia, Japan, and Korea driving new builds. The construction market in Asia-Pacific is projected to see a CAGR of 13.3% from 2025 to 2030. Grand View Research

-

Europe is investing strongly in local data sovereignty, AI datacenter hubs, and green infrastructure.

-

Latin America and Middle East & Africa are emerging but face power and regulatory constraints; yet demand for digital infrastructure and cloud expansion is pushing growth in key hubs.

-

Edge deployments are geographically dispersed, often in remote or under-served locations linked to telecom towers, rural areas, or urban micro-hubs.

Market Size and Factors Driving Growth

Current Valuation & Forecasts

- The global data center construction market was valued at USD 48.39 million in 2024 and is expected to reach USD 95.72 billion by 2032

- During the forecast period of 2025 to 2032 the market is likely to grow at a CAGR of 8.90 % primarily driven by the increasing demand for cloud services, AI technologies, and digital transformation initiative

These variances reflect differences in definitions (investment value, infrastructure scope, geographic coverage) and forecasting methodologies.

Given multiple projections, a reasonable outlook is that by 2035 the data center construction market might reach USD 400–500 billion+, driven by AI, cloud, edge, and sustainability demands.

Key Growth Drivers

-

AI and HPC workloads pushing higher power densities and new builds. McKinsey & Company+1

-

Cloud, 5G/IoT proliferation, and edge computing demand broader geographic distribution of data centers.

-

Digital transformation across industries: Every sector demands scalable compute and storage.

-

Hyperscaler investment strategies: Large cloud firms systematically expand new data center campuses globally.

-

Green energy and ESG imperatives: Projects now embed renewables, energy reuse, efficiency, and carbon targets from the outset.

-

Modular and prefabricated construction reducing time, cost, and risk.

-

Regulations and data sovereignty: Laws requiring local data storage prompt local builds.

-

Telecommunications expansion: Telcos building data centers for edge or mobile traffic aggregation.

Opportunities in Emerging Regions

-

Rapid adoption in India, Southeast Asia, Latin America, Middle East & Africa as data penetration increases and local cloud demand grows.

-

Edge data center construction in rural and remote zones, particularly with 5G rollout.

-

Specialization in AI-optimized green campuses with efficient cooling, waste heat reuse, and renewable integration.

-

Retrofits and densification in older data centers to improve power usage effectiveness (PUE) and capacity.

-

Public-private partnerships where governments subsidize data infrastructure to boost digital economies.

Conclusion

The Data Center Construction Market is entering a period of sustained expansion, driven by AI, cloud, edge computing, and digital transformation. With a baseline of approximately USD 240–280 billion today and forecasts indicating a move toward USD 400–500 billion+ by 2035, the market offers considerable growth potential. The most compelling opportunities lie in high-density AI datacenters, modular and edge deployments, sustainability-enabled designs, and emerging geographies.

Stakeholders—developers, operators, technology vendors, energy providers, regulators—must align on strategies that manage cost, speed, power constraints, regulation, and future-proofing. Successfully delivered projects will integrate resilience, efficiency, and flexibility from inception.

Frequently Asked Questions (FAQ)

Q1: What was the value of the global data center construction market in 2024?

A1: According to Grand View Research, it was about USD 240.97 billion. Grand View Research Other estimates (e.g. Mordor) suggest ~ USD 281 billion by 2025. Mordor Intelligence

Q2: What is the expected CAGR for the period 2025–2030?

A2: Grand View projects 11.8% CAGR for 2025–2030. Grand View Research Mordor projects 7.3% CAGR for 2025–2030. Mordor Intelligence

Q3: Which region leads in data center construction?

A3: North America holds a dominant position, accounting for more than 40% share in 2024. Grand View Research+1 Asia-Pacific is forecasted to have the highest growth rates. Grand View Research+1

Q4: What infrastructure segment dominates the spending?

A4: Electrical infrastructure (UPS, generators, switchgear, power distribution) captures significant share, with mechanical cooling and power-backup systems also major cost centers. Mordor Intelligence+2Grand View Research+2

Q5: What is driving demand for new data centers?

A5: Key drivers include AI workloads requiring high power density, cloud expansion, edge computing, industry digital transformation, data sovereignty laws, and performance demands from 5G/IoT. Research Nester+3McKinsey & Company+3JLL+3

Q6: What major risks does this market face?

A6: Power constraints, regulatory and permitting delays, supply chain lead times, capital intensity, obsolescence risk, high operating expenses, and sustainability compliance.

Browse More Reports:

Europe Benign Prostatic Hyperplasia Devices Market

Middle East and Africa Benign Prostatic Hyperplasia Devices Market

North America Benign Prostatic Hyperplasia Devices Market

Europe Bio-Based Lubricants Market

North America Bio-based Lubricants Market

North America Bioherbicides Market

Asia Pacific Bioherbicides Market

Europe Bioherbicides Market

North America Bio-Implants Market

Europe Bio-Implants Market

Asia-Pacific Bio-Implants Market

North America Biomarkers Market

Asia-Pacific (APAC) Biomarkers Market

Europe Bonsai Market

Asia-Pacific Bonsai Market

About Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- [email protected]